Stamp Duty – What are the latest changes?

26.01.18Stamp Duty has been one of the most talked about taxes in recent years and love it or loathe it, let’s face it most loathe it, it is nevertheless here to stay. For the latest up-to-date changes to stamp duty, take a look at our guide to stamp duty.

After having stayed the same for a number of years, the much-maligned “slab” system was changed in 2014 by George Osborne to a more progressive tiered system, which was followed a year later by a further change whereby those purchasing a second home, (or third, fourth etc) would have to pay a further 3% surcharge above the standard rate at any price.

Therefore, if you are buying a further property without selling the property in which you currently reside you will be charged the additional 3%. This applies to all properties purchased whether in personal names or under a Limited Company.

You are able to get this additional 3% refunded if your old home is then subsequently sold within 3 years of buying your new home.

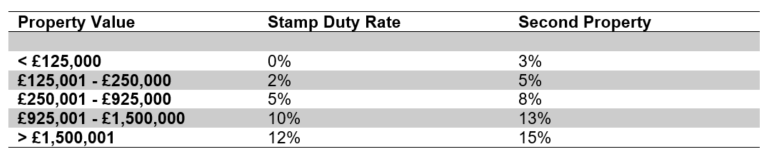

For most people then, Stamp Duty rates currently stand as follows and apply to each portion of the price:

For example, someone purchasing at £500,000 will pay:

0% on the first £125,000 = £0

2% on the next £125,000 = £2,500

5% on the final £250,000 = £12,500

Total Stamp Duty to pay = £15,000

Latest Changes for First Time Buyers

Last year the new Chancellor changed things round again, but only for First Time Buyers and only if you are buying a property up to £500,000.

If you meet both these criteria then there is now no stamp duty to pay on the first £300,000.

For example, someone purchasing at £500,000 will pay:

0% on the first £300,000 = £0

5% on the final £200,000 = £10,000

Total Stamp Duty to pay = £10,000

In other words, First Time Buyers can now save up to £5,000 on the cost of Stamp Duty.

Please note that for First Time Buyers Purchasing over £500,000 there is no saving and the standard rates apply.

Hopefully, this is all a little clearer, but we are always on hand for any questions you have about this.

Happy house hunting.

Written by Andrew Montlake

Andrew Montlake, better known as Monty, began his journey with an Hons degree in Economics & Politics before starting in the mortgage industry in February 1994. As a main founder of Coreco in 2009, he successfully grew the brand, marketing, and communications, and was made MD in 2019 focussing on the overall vision, strategy, and culture of the company. As Coreco’s media spokesperson, Andrew can often be seen or heard on TV and radio as well as regularly commenting in the national, local, and trade press. He is the author of this acclaimed Mortgage Blog and is well-known for his social media, podcasts, and public speaking. Andrew is now proud to serve as Chairman of the Association of Mortgage Intermediaries, (AMI) as a cheerleader for the Mortgage Industry as a whole and continues to work at the coal face, writing mortgage business and advising clients.

Read more posts by Andrew